A remodel or ADU in Los Angeles is a six-figure decision for most homeowners, and how you pay for it matters almost as much as what you build. The right financing keeps the project moving and the monthly cost manageable. The wrong fit stalls the job or stretches your budget.

This is a plain overview of the main options homeowners use in LA. It is general information, not financial advice, so confirm the details with a lender and a tax professional before you commit.

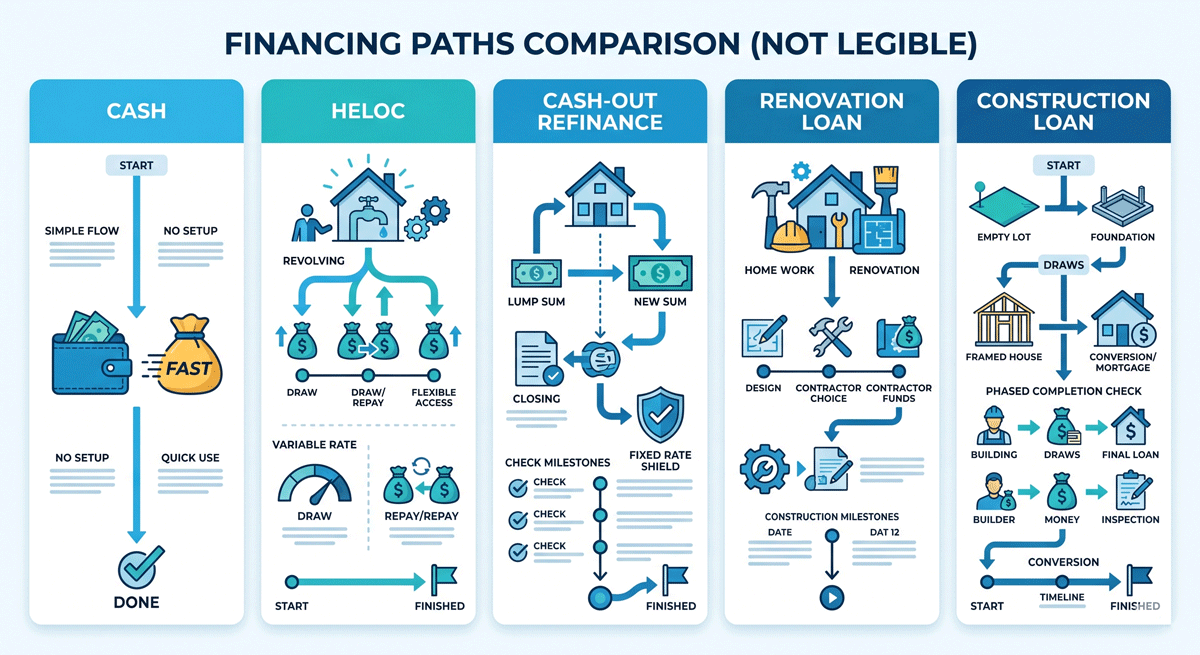

Paying cash versus financing

Paying cash avoids interest and closing costs and keeps the project simple. The tradeoff is liquidity; draining savings into a remodel leaves less cushion for the surprises that older homes tend to produce. Many homeowners use a blend, paying part in cash and financing the rest to keep a reserve in place.

Home equity line of credit and cash-out refinance

If you have built equity in your LA home, two of the most common tools draw on it.

HELOC

A home equity line of credit works like a revolving credit line secured by your home. You draw what you need as the project progresses and pay interest only on what you use, which suits phased work. Rates are usually variable.

Cash-out refinance

A cash-out refinance replaces your existing mortgage with a larger one and gives you the difference in cash. It can make sense when you want a single fixed payment, though it resets your mortgage and only pencils out in certain rate environments.

Renovation loans

Renovation loans roll the purchase or refinance and the remodel budget into one loan, based on the home’s expected value after the work is done. Two common programs are the FHA 203(k) and the Fannie Mae HomeStyle Renovation loan. They are useful when you do not yet have enough equity to fund the work outright, because they lend against future value rather than current value.

Construction and ADU-specific loans

Larger projects, including a detached ADU or a full rebuild, often use a construction loan or a construction-to-permanent loan. These release funds in stages as the work hits milestones, then convert to a standard mortgage when the project is complete. They typically require about 20 percent down, solid credit, detailed plans and a confirmed builder before approval.

For ADUs specifically, some lenders now offer products that underwrite against the future value the ADU will add and the rent it will produce, which can unlock more borrowing capacity than equity alone. Availability changes, so ask a lender what current ADU programs exist.

Contractor and in-house financing options

Many homeowners also use financing arranged through their builder. Ground Up Builders maintains a finance page with current options for clients who would rather not manage lender shopping on their own. This can be a convenient path, and it is still worth comparing the terms against a HELOC or renovation loan.

How to choose

The best fit depends on a few simple questions. How much equity do you have today? Do you want a fixed payment or flexible draws? Is this a phased remodel or a single large build? And how long do you plan to stay in the home? A short answer for many LA homeowners: HELOCs suit phased remodels with existing equity, renovation loans suit buyers and lower-equity owners, and construction loans suit ADUs and rebuilds.

What lenders want to see

Whichever route you take, lenders generally look for a reasonable credit score, stable income, manageable existing debt, and a clear scope of work with a builder estimate attached. Having a detailed, itemized estimate ready, the kind a complete builder quote provides, makes the lending conversation faster and smoother.

Frequently Asked Questions

What is the best way to finance a remodel in Los Angeles?

There is no single best option. Homeowners with equity often use a HELOC or cash-out refinance, buyers and lower-equity owners use renovation loans, and large projects use construction loans. The right fit depends on your equity, your preference for fixed or flexible payments, and the project size.

Can I get a loan specifically for an ADU?

Yes. Construction and construction-to-permanent loans are common for ADUs, and some lenders offer ADU-specific products that underwrite against the future value and rental income the unit will add. Program availability changes, so ask a lender what is currently offered.

What is the difference between a HELOC and a renovation loan?

A HELOC draws against the equity you already have and lets you borrow flexibly as work progresses. A renovation loan, such as an FHA 203(k) or Fannie HomeStyle, lends against the home’s value after the work is done, which helps when you do not yet have enough equity.

How much do I need for a down payment on a construction loan?

Construction and construction-to-permanent loans typically require around 20 percent down, along with good credit, detailed plans and a confirmed builder. Exact requirements vary by lender.

Does Ground Up Builders help with financing?

Ground Up Builders maintains a finance page with current options for clients. It can be a convenient path, and we always encourage comparing the terms against a HELOC or renovation loan so you choose what fits best.

| Planning a remodel or ADU and weighing how to pay for it?

Start with a clear, itemized estimate. Ground Up Builders provides free estimates across Greater Los Angeles, Orange County and Ventura County, which is exactly what lenders want to see before approving your project. Visit groundupbuilders.com | Free estimates, no obligation. |